TAMPA -- Hurricane season is here, so this is a good time to find out exactly what your hurricane insurance covers and, more importantly, what it does not cover.

Insurance Coverage Attorney Amy Boggs says, in her experience, many homeowners simply don't know.

"The unfortunate thing is this stands between you and financial devastation in the event of a hurricane loss," Boggs said.

How Hurricane Deductibles Work

Many people, for example, don’t know how a hurricane deductible works.

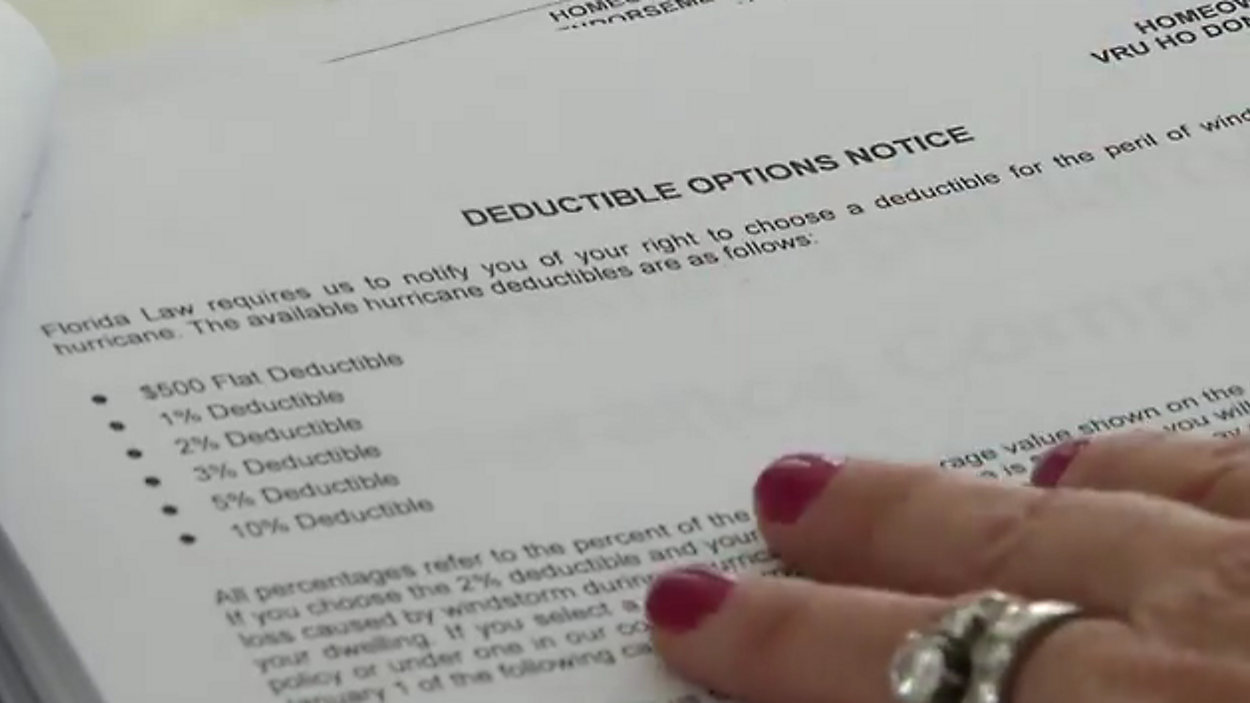

It's not the same as the deductible on a regular home insurance claim.

For hurricane damage, you choose the amount you want to pay when you buy your policy. It can be either $500, one percent, 2 percent, 3 percent, 5 percent or 10 percent-- but here’s where many people get confused—that percentage is of your total policy coverage, not your claim amount.

"So people said, 'Oh, I can do a 5 percent hurricane deductible. If I have a $15,000 roof claim in a hurricane, I can afford to pay 5 percent of that. It’s only $750,' " Boggs said, explaining how homeowners misunderstood. "The truth of the matter is if they have a $200,000 policy, which is pretty standard, they would wind up paying $10,000 towards that roof," she added.

"Oh wow, that's horrible," said homeowner Julie Jones, when we explained how the hurricane deductible works.

What’s NOT Covered?

Another important thing to understand is what your hurricane coverage does not cover. Some big exclusions include your pool enclosure and your car port. If you want those covered, you have to pay extra.

"It's changed over the years," said homeowner Mike Merino. "It wasn’t like that 20 years ago. The insurance has gone up and you’ve got less coverage."

Another thing that many people don't realize is a standard policy does not cover bringing your home up to code if you need repairs. You also have to buy extra coverage for that. It's called "Law and Ordinance" coverage, and it could prove especially important if you have an older home.

Right to repair clause

Another tricky provision that might be lurking in your policy is something called a "Right to Repair" clause. This is where the insurance company can choose to repair the home, instead of cutting you a check for the estimated amount to do the work. In some cases, the policy actually calls for you to use the company’s contractor, so you have no say in who repairs your home.

Insurance companies might give you a small discount in exchange for this, but Boggs says it's not worth it.

"Don't do it!" she advised. "You're captive to who they want you to use and those folks, of course, have a vested interest in getting the claims done as cheaply as possible."

Boggs says she has represented many clients who’ve had bad experiences with these Right to Repair provisions.

"Delays, shoddy workmanship; and I see where they (the insurance company)won’t agree on what actually needs to be done," she explained. "You basically get a $20 discount on your premium in exchange for this horrible situation on the back end."

Worst of all, many homeowners don't even realize the Right to Repair clause is in their policy.

Boggs recommends you shop around for new coverage if your policy has a provision like this that can force you to use the insurance company’s contractor.

The best advice for all homeowners, now that hurricane season is here, is to take out your hurricane policy and read it over. Make sure you understand exactly what your coverage is.

Hopefully you won't need it, but if you do, it’s best to be prepared.